Africa: the media and technology challenges and opportunities across an expanding market

Globecast covers the continent of Africa from our office in the Middle East – which looks after Northern Africa and our base in South Africa. Here in South Africa, we work across Sub-Saharan Africa, alongside Lionel Antoine, Sales for Africa, who’s based in Paris and is part of our team. He looks after the French-speaking countries, where we have had considerable recent successes.

My role has an emphasis on sales and business development. In a time of technology change and cost cutting, I’m always pushing our team to challenge the way we do things; to look at new technology and practices to see if we can’t improve the quality of our services and at the same time make them more cost effective to our clients.

One of the biggest challenges is digital disruption. Technology is massively transforming the media industry. It has in the past but while the jump from say, the introduction of sound to the move from B&W to colour, and from SD to HD to 4K, might have required retooling and capital outlay, the landscape of the industry was largely unchanged. Digital transformation has lowered the barrier to entry as well as blurring the lines between the activities of existing players.

The space that was dominated by TV for decades has become more crowded. We now have TV companies, telcos, OTT operators, movie studios, sports federations and social networks all competing for the same subscriber or advertising dollar.

Throw in eSports, gaming and music streaming and it is even more crowded. Netflix has been quoted as saying that Fortnite is a bigger threat than other studios or production companies. It puts pressure on our historic customers but also requires us to look for more inventive ways to deliver their content and serve the digital needs of the new entrants.

Digital revenue is said to be growing as much as ten times faster than non-digital and increasingly companies are looking for a bundled social media, e-commerce and entertainment offerings. The major players aren’t much concerned with how they reach an audience as long as they own that audience. A DTH satellite provider would welcome the lower costs of internet delivery as long as it’s reliable and the consumer was still accessing the content through a platform they owned. One DTH provider in our region is now offering its viewers subscription packages bundled with unlimited internet connectivity.

Digital platforms have the advantage of giving companies access to an individual’s data, tastes, habits and usage and that sort of information is a compelling factor in terms of ad revenues. It’s now believed that in Africa Internet advertising will overtake TV advertising within two years. We have worked on widening our services suite to include the delivery of video content over the internet. This ranges from a simple streaming of a channel from A to B to the provision of an all singing and dancing turnkey OTT video platform.

On the delivery side, we’ve downlinked or taken in house content ranging from Tier 1 sports to business channels and streamed them to VOD platforms around the world. We’ve streamed channels from Europe to DTH headends in South Africa. And we’ve streamed channels and live sports and other events from the stadium or point of origin direct to the consumer.

On the OTT side we have provided VOD only platforms and platforms that include a combination of VOD content and live, linear channels. The range of services includes: ingestion, transcoding, adaptive bit rates, HLS, DASH, TVOD, SVOD, ADVOD, CMS, CRM, DRM, analytics, CDN, etc. etc.

We’ve been involved in the launch of six different platforms in recent years and also provide ‘marketplace solutions’, which enables a customer to manage a VOD site and also allows their subscribers to upload their own content.

It’s been said that traditional television is dying. Maybe, but, if so, it’s a very slow, lingering death. OTT platforms may be becoming more and more popular but linear TV is still very relevant.

In Africa, the ability to source local content on international OTT platforms might be limited, meaning people will stick with a linear channel that’s giving them the content they want in the language they want. Also, many OTT platform operators in Africa will request live channels are carried and they are generally the local channels from a particular country or 24-hour news channels.

In Africa, second screen activity is growing but still limited pretty much to messaging. A recent study showed that in Nigeria 52% of smartphone owners used their phones while watching TV and in South Africa that number rises to around 70 per cent.

Monetisation still appears to be an issue with OTT services in South Africa and there are probably very few operators turning a profit. We’ve seen platforms fail because they are offering Hollywood content where the studios will take the lion’s share of any consumer spend. So, it’s the type of content and the cost of content that’s critical. In our experience, if you’re offering niche material or local content that’s not readily available elsewhere, you have more chance of success.

If you’re a broadcaster with your own library of content or content to which you own the digital rights, then you probably should be looking at an OTT platform. The costs are low, you can bring your back catalogue out of the vault and at the same time develop alternative revenue streams and go some way to future-proofing your business.

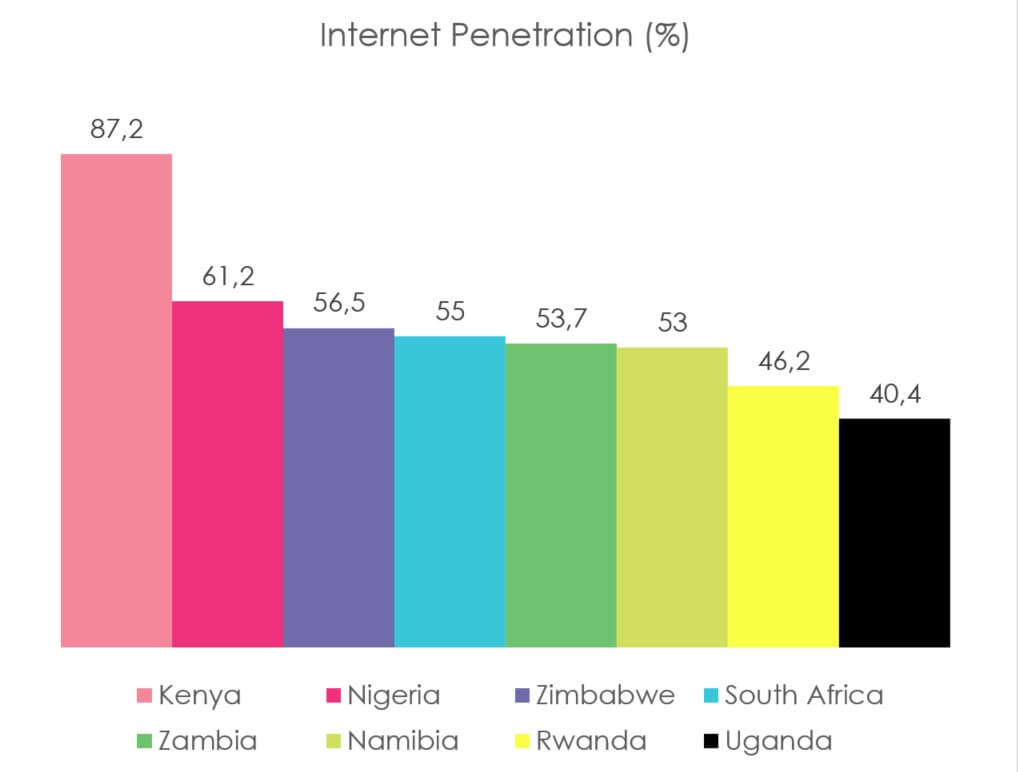

As a continent, Africa is far from homogeneous. While general trends may be similar, some countries are more advanced in terms of internet penetration or may have more sophisticated broadcasting or advertising industries. While there’s a common trend – the desire for local content – by definition that content varies. One of the major variations is the regulatory landscapes, with many countries pushing laws that make it difficult for international companies to gain any meaningful traction without a local partner.

In terms of COVID, the biggest consequences have been the drop in advertising spend and the restrictions on sport and live shows. This has impacted heavily on all contribution business. While advertising is showing signs of picking up, the downturn in live events and shows is likely to continue into next year as many international shows due to be shot in South Africa in early 2021 have already been cancelled. What we have seen is an immediate demand for pop-up channels – mainly educational – and we were able to handle the playout of these channels as well as delivery to respective headends.

We are working closely with all our customers to provide as much business and technical guidance in what are currently challenging circumstances for so many of us. We are here to help.