The word “broadcast” originally defined the technology behind radio and video transmissions, but it soon came to describe a whole industry and its stakeholders.

As the technology evolved, so did the overall ecosystem; the stakes grew with new delivery methods developed and new players appearing, continue to shake up the industry landscape.

In terms of popularity, broadcast is now being replaced by the phrase Media Entertainment and Technology (MET) to refer to our changing industry. And unless you’ve been lost on Planet 51 the past few years, you must have heard – or thought – at least once: is the term broadcast simply outdated?

Here are seven facts to help you decide if MET is overtaking broadcast.

1. The future belongs to the young

For many years, TV viewing was often considered a social gathering, uniting family and friends in front of a single screen.

With the fragmentation of devices and consumption, viewers in the 2010s now demand far more personalization alongside recommendation services. People are more eager to choose specific content suited to them rather than watch traditional TV programmes via a schedule.

Over the next five years, 20% of users may stop watching linear TV, rather watching personalized pay-TV offerings. Considering that Gen Z and Millennials spend less time per day watching linear TV, this is no big surprise. But that might mean big trouble for traditional broadcasters.

2. Infinite content is king

As stated by Cisco in its Forecast and Trends whitepaper, by 2022, 82% of all IP traffic will be video. Video is now the new frontier for media companies as it helps drastically increase user numbers and revenues.

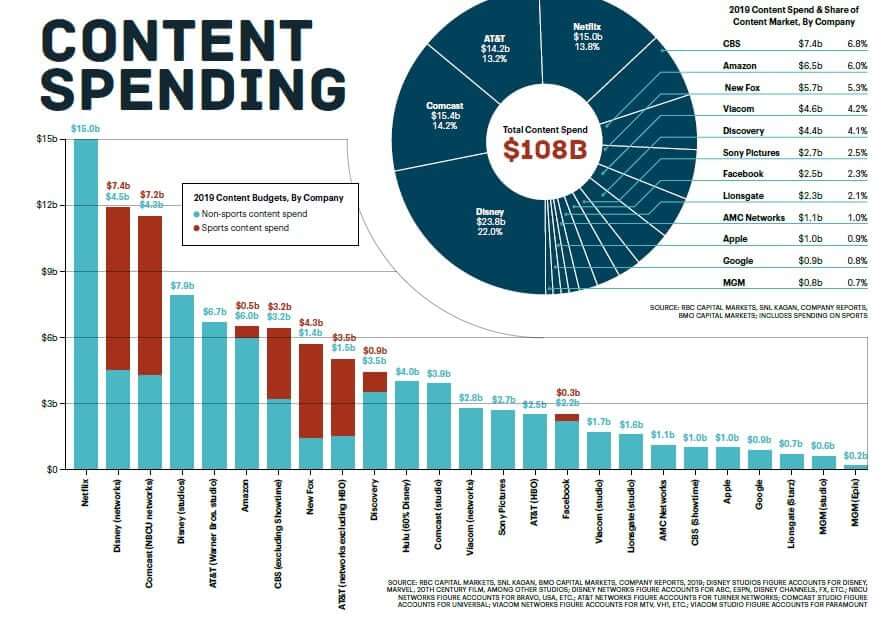

No wonder the FAANGs (Facebook, Apple, Amazon, Netflix and Google) have increased by 30% their investment in original content in the past few months. And when we’re talking investment, we’re talking big numbers. Netflix, for instance, was already set to produce more content than any broadcaster or film studio in the world in 2018 and will invest up to $15bn bin 2019.

Although big players like Disney, or smaller thematic broadcasters, may not feel threatened, medium-sized traditional broadcasters are under a lot of pressure to invest more in video content.

Source: FlatPanelHD.com

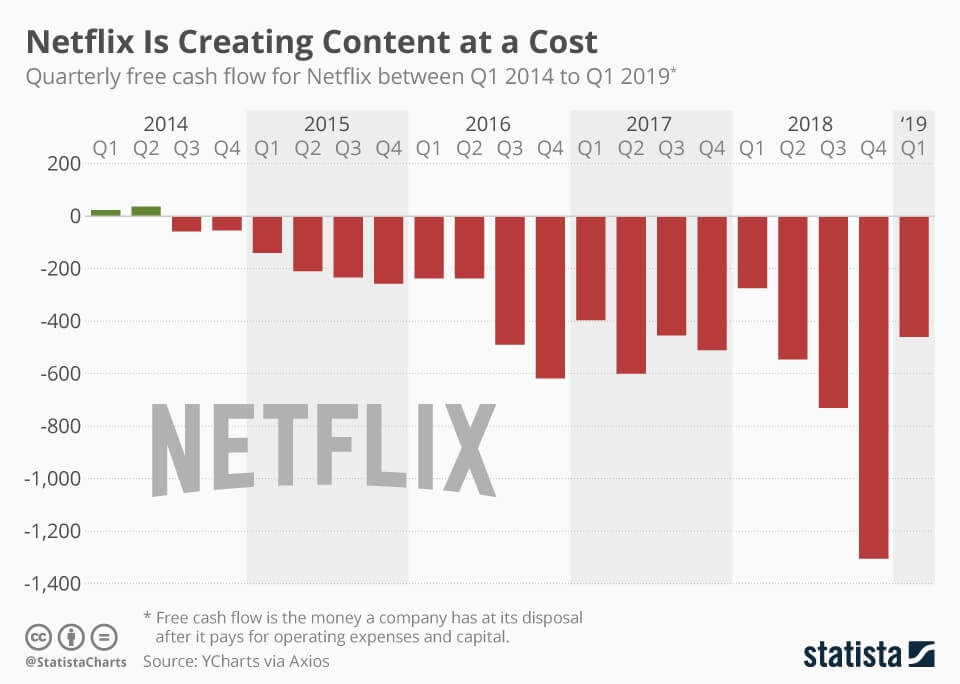

3. Creating content has a cost

If infinite content is king, getting close to the throne requires not only massive investment but also big sacrifices; the new media companies know well what it takes.

But even though its subscriber base is still growing worldwide, by the end of 2019 Netflix is expected to record a $3.5bn free cash-flow deficit. The company has already sustained a $400m loss in Q1 2019.

Digital TV Research also forecasts that pay-TV revenue will decrease significantly, falling from $202bn in 2017 to $183bn in 2023.

GAAFs are showing some signs of weakness lately in what is a highly competitive market and this may suggest that the golden age of new entrants is coming to an end, or we’ll see consolidation of service providers.

It’s difficult to say at this point weather to increase viewership companies should invest so much in content creation.

Q: We all know there’s a cost, but the question is how much?

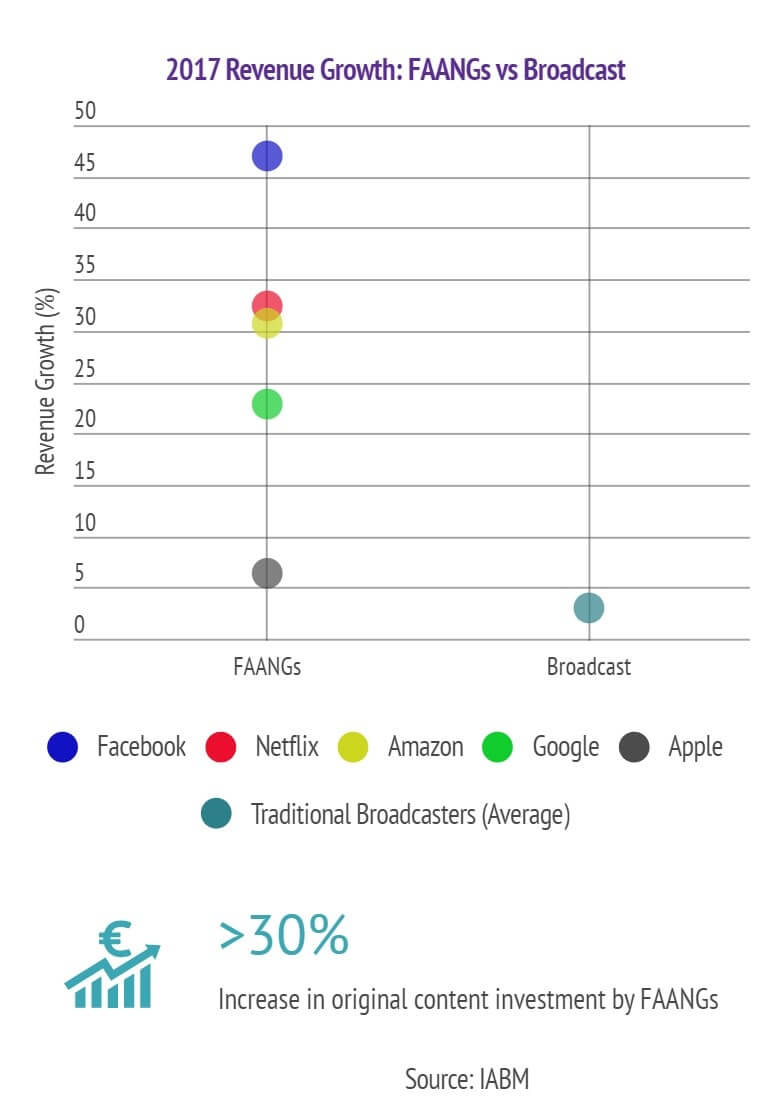

4. FAANGs are putting more pressure on broadcast industry

Nothing new here, but the trend keeps growing. The FAANGs, seizing the video opportunity, go direct to consumers, bypassing traditional distribution channels to increase both their audience and accelerate their return on investment (ROI) from advertisement/subscription revenues.

They now have a higher revenue growth than traditional broadcasters and that growth in revenue can be startling. You know how important growth is in our world!

See #iabm for more insights on key trends driving change in the broadcast and media sector

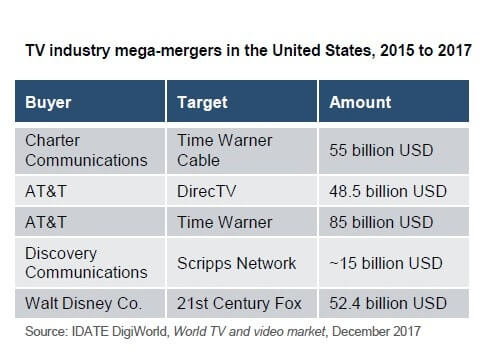

5. Broadcasters are retaliating

Strength lies in numbers. Traditional media companies are reinforcing their position, expanding geographically and collaborating to reduce the pressure coming from FAANGs and other new media companies.

Thus, in March 2018, four tier-1 European commercial broadcasters united under The European Broadcaster Exchange (EBE) banner to find new ways to develop online TV and video advertising to counterbalance Google and Facebook’s supremacy in this key domain.

Others cooperative initiatives arise via possibilities such as blockchain. Groupe Média TFO, a Canadian media company, is now partnering with traditional broadcasters on a proof-of-concept to find means to fight piracy and fake news but also to secure right payments and increase revenues with smart contracts.

These are a few examples, amongst many, showing traditional broadcasters’ fierce determination to have a piece of the growth cake.

6. Broadcasters are also going direct to consumers

Many players today provide their own OTT offerings, focusing their efforts directly on dedicated platforms.

Disney removed its catalogue from Netflix to launch a cheaper and competitive SVOD platform by the end of 2019. AT&T might provide the same around its own Time-Warner content within the year, too. Warner Media and NBCU will be launching their SVOD platforms next year.

If you’re looking to deploy OTT video services, then get in touch as we have comprehensive, flexible and cost-effective solutions, including server-side dynamic ad insertion. Reach us to start discussing additional audience and revenue opportunities for your company

With the ever-growing number of SVOD platforms, the question remains whether subscribers will continue to be willing to pay multiple providers and subscriptions to view the content they want. So far, the answer has been yes, but for how long?

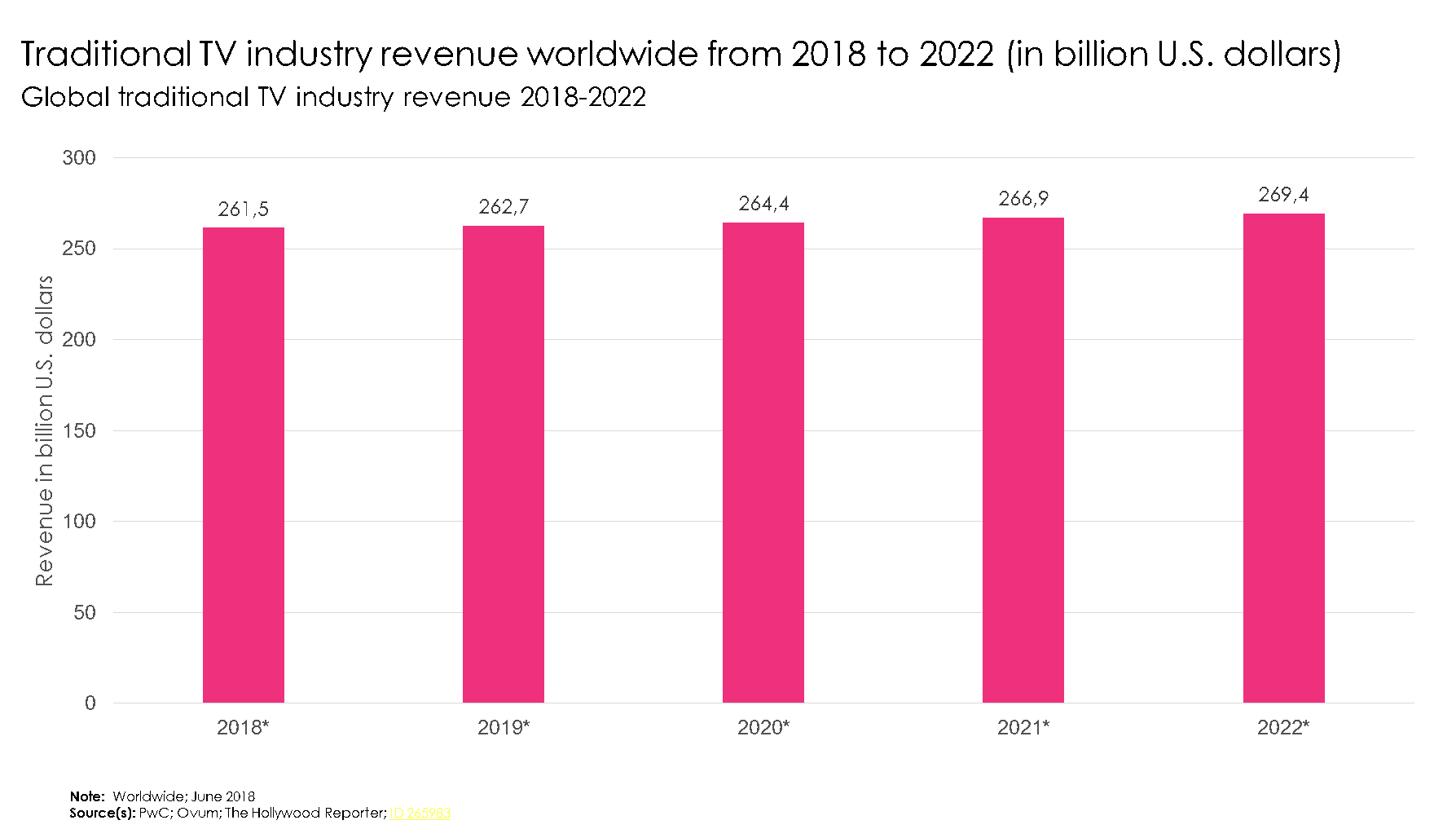

7. Linear TV consumption still accounts for the largest share

Though we spend a lot of time talking about SVOD, linear TV is still the most popular way to watch video around the world

Against all odds, screen time and traditional TV revenues are generally stable worldwide. As per an IDATE DigiWorld December 2017 report, advertising revenues are also expected to grow at a steady pace and reach globally €184.5bn in 2021 vs. €171bn EUR in 2016.

35 years later we all know that video didn’t kill the radio star. Similarly, there’s a high chance that broadcast and MET will grow together in the coming years and will quite merge in the end…

If you still have doubts about this and will be at IBC 2019, there are three conference sessions that may interest you: Is There Still Life In Linear Broadcasting?; Digital Publishing: The New Broadcasters; and Content Beyond Broadcast.

Of course, we’ll be at IBC and hope to see you on our stand 1.A29 to share our thoughts on broadcast and MET. You can book a meeting here or simply show up at the booth!